Planning a home renovation in 2026 often means deciding how to pay for the project. Whether you’re remodeling your kitchen, updating a bathroom, replacing your roof, or building an outdoor living space, choosing the right financing option can save you thousands of dollars over time. Two of the most popular choices are a Home Equity Line of Credit (HELOC) and a personal loan.

While both provide access to funds, they differ significantly in interest rates, repayment terms, approval requirements, and financial risk. Understanding these differences can help homeowners select the financing solution that best fits their renovation goals.

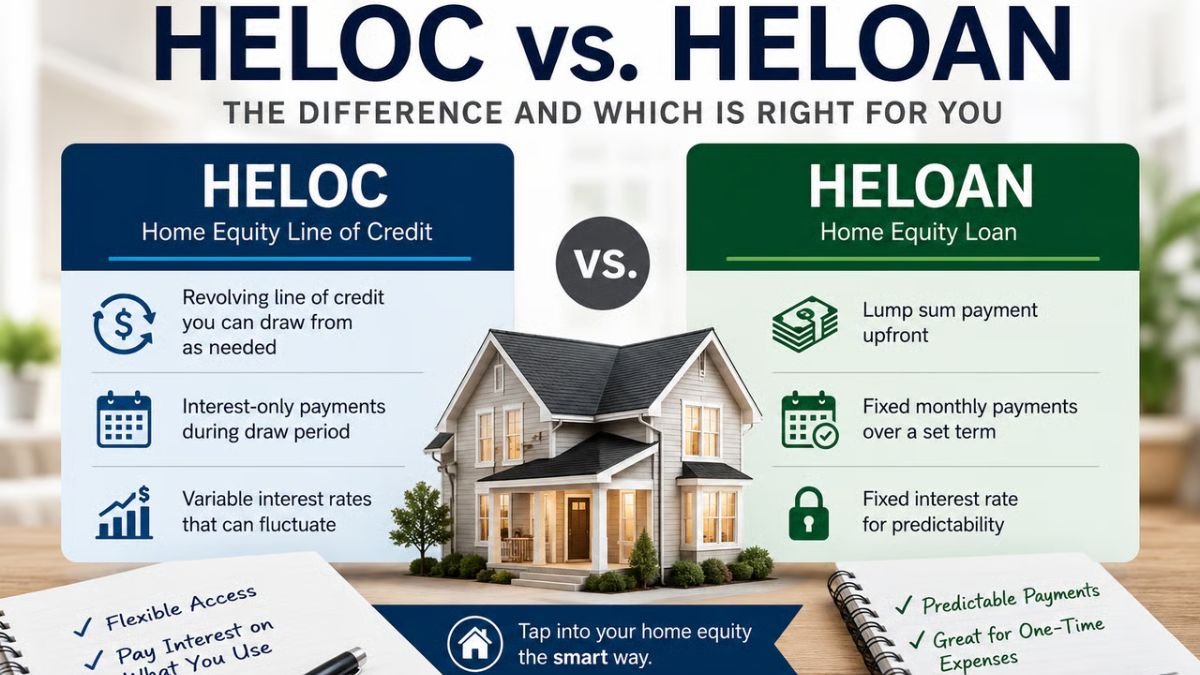

What Is a HELOC?

A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity they’ve built in their property. Instead of receiving a lump sum, borrowers gain access to a revolving credit line that they can draw from as needed during the draw period.

Most lenders allow homeowners to borrow up to 80% to 90% of their home’s available equity, depending on credit qualifications and lending policies.

One of the biggest advantages of a HELOC is flexibility. You only pay interest on the amount you actually borrow rather than the full approved credit limit.

How Personal Loans Work

Unlike a HELOC, a personal loan is unsecured, meaning it doesn’t require your home as collateral. Once approved, you receive the full loan amount upfront and repay it through fixed monthly payments over a predetermined term.

Personal loans have become increasingly popular for medium-sized renovation projects because borrowers know exactly how much they’ll owe every month.

Loan amounts generally range from a few thousand dollars up to $100,000, depending on the lender and the borrower’s financial profile.

Interest Rates in 2026

Interest rates remain one of the biggest deciding factors.

HELOCs generally offer lower starting interest rates because the loan is secured by your home. However, most HELOCs carry variable interest rates, meaning monthly payments can rise or fall as market rates change.

Personal loans usually have fixed interest rates. Although they often begin slightly higher than HELOC rates, borrowers benefit from predictable monthly payments throughout the loan term.

For homeowners concerned about future rate increases, the stability of a fixed-rate personal loan can provide valuable peace of mind.

Which Option Is Better for Home Renovations?

The answer depends largely on the size and timeline of your renovation project.

A HELOC may be ideal if:

- Your renovation will occur in multiple phases.

- You want flexibility to borrow only what you need.

- You have substantial home equity.

- You’re comfortable with variable interest rates.

A personal loan may be better if:

- You know the exact project cost.

- You want predictable monthly payments.

- You don’t have significant home equity.

- You prefer not to use your home as collateral.

Advantages of a HELOC

A HELOC offers several benefits for homeowners tackling larger remodeling projects.

Lower interest rates often make borrowing less expensive compared to unsecured financing.

Flexible access to funds allows homeowners to pay contractors, suppliers, and unexpected expenses as they arise.

Many HELOCs also feature longer repayment periods, helping reduce monthly payment amounts.

Because the credit line remains available during the draw period, homeowners can finance multiple improvement projects without applying for additional loans.

Advantages of Personal Loans

Personal loans offer simplicity and certainty.

The fixed repayment schedule makes budgeting much easier since payments never change.

Approval is generally faster than a HELOC because no home appraisal or equity verification is typically required.

Since your property isn’t used as collateral, there’s no direct risk of foreclosure if financial difficulties arise, although missed payments can still damage your credit score.

Many online lenders can approve and fund qualified borrowers within a few business days.

Potential Risks to Consider

Both financing options carry important risks.

With a HELOC, your home secures the loan. Failure to make payments could ultimately result in foreclosure. Variable interest rates also create uncertainty if market rates continue changing.

Personal loans generally have higher interest rates than HELOCs, especially for borrowers with average or poor credit. Monthly payments may also be higher because repayment periods are often shorter.

Before choosing either option, homeowners should carefully compare total borrowing costs rather than focusing solely on the advertised interest rate.

How to Choose the Right Financing Option

Ask yourself several important questions before applying:

- How much money do you actually need?

- Is your renovation cost fixed or likely to change?

- How much home equity have you built?

- Can your budget handle possible interest rate increases?

- Would fixed monthly payments help your financial planning?

If you’re completing a large custom renovation over several months, a HELOC often provides greater flexibility. For smaller, well-defined projects with fixed costs, a personal loan may deliver greater financial certainty.

Choosing between a HELOC for home renovations vs. personal loans ultimately depends on your financial situation, available home equity, and risk tolerance. A HELOC typically offers lower borrowing costs and flexible access to funds, making it attractive for extensive remodeling projects. Personal loans, meanwhile, provide fixed payments, faster funding, and eliminate the need to use your home as collateral.

Before making a decision, compare offers from multiple lenders, review all fees, understand repayment terms, and calculate the total cost over the life of the loan. Taking time to evaluate both options can help ensure your renovation improves your home without creating unnecessary financial stress.

FAQs

Is a HELOC cheaper than a personal loan?

In many cases, yes. HELOCs generally offer lower starting interest rates because they are secured by your home’s equity. However, rates are often variable.

Can I get a HELOC if I recently purchased my home?

Possibly, but you’ll usually need sufficient home equity. Many lenders require homeowners to have built meaningful equity before qualifying.

Which loan is easier to qualify for?

Personal loans are often easier and faster to obtain because they don’t require home equity or property appraisals. Approval primarily depends on your credit score, income, and debt-to-income ratio.